Equity finance in the United States operates within a relatively closed market environment, governed by stable regulations with known participants, settlement and collateral profiles. These conditions produce fewer surprises than more open financial systems that depend on multi-currency capital flows or complex macroeconomic linkages. This is important for forecasting models. A narrower set of external shocks means that historical scenarios map with less noise onto present conditions. By training algorithms with data reflecting similar structural regimes, analysts can refine their forecasting models, reducing the margin for error. Equivalent market structures enable thoughtful calibration and continuous improvement, strengthening predictive power.

Consider the nature of market behavior in U.S. equity finance. Lenders and borrowers follow established protocols, while the market is bounded by available share inventory and regulatory capital rules. Stock prices and overnight bank funding rates are the main external influences. The underlying economics may not be free of forecast surprises, but the potential range of deviations narrows. Could better training of GenAI models in the more restricted domain of securities finance act to enhance model reliability and incremental alpha? In a word, yes.

Relevant Period Training

By capturing patterns of borrower behavior that recur across comparable conditions in a closed market, forecasters can fine-tune their models to isolate the features of emerging trends. Research supports this notion; when models echo the historical realities of borrowers, the resulting projections reflect underlying market truths rather than random noise. This method leverages known patterns, minimizing anomalies that stem from unpredictable global conditions.

Training data drawn from relevant prior periods or scenarios has practical benefits. Analysts can segment historical periods that closely resemble current conditions, extracting insights from times when participant activity and results parallel those of today. Instead of muddling projections with data from drastically different epochs, one can strategically weigh outcomes from carefully selected windows. By focusing on data reflecting consistent structures, models generate expectations that mirror genuine market responses. Relevant period training inches models closer to accurate forecasts that clients can trust.

Streamlined Model Governance

Deployment and calibration of GenAI models is governed by compliance policies, processes, and practices. It ensures that models are not only aligned with organizational goals and comply with regulatory requirements, but also operate in a way that is ethical, fair, and transparent.

In a stable, closed environment such as the cash-collateralized U.S. stock loan market, modelers using relevant period training face fewer anomalies, thereby creating a baseline for explainability, with more straightforward validation and verification steps. Periodic audits become more routine (and less contentious) without the complexity, for example, of rapid shifts in cross-border currencies and capital flows. Could better training rigs and lower recalibration complexity translate into lower administrative burdens for firms? Indeed, model governance frameworks, often bloated with diverse scenario testing requirements, can focus bias tests on security-specific, currency-neutral benchmarks. This refined approach lowers overall compliance costs and saves time. By tailoring governance protocols, participants ensure that oversight remains thorough yet cost-efficient, further enhancing operational resilience and trust.

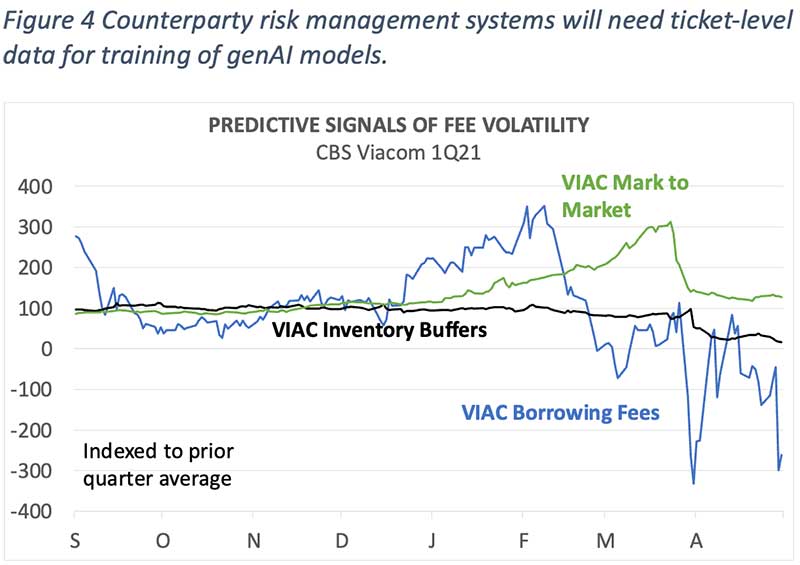

Models are better trained by focusing on what truly matters—patterns of trade direction, magnitude, and capital velocity observed in similar periods. This thoughtful data selection allows analysts to discard irrelevant inputs that distort the big picture. The results are cleaner forecasts that tell a more coherent story of where the market may be headed.[1] By applying these insights, forecasting becomes less about guesswork and more about systematic analysis grounded in historical parallels. In this controlled context, what if we move beyond aggregate data and turn to granular ticket-level inputs? Ticket-level data reveal the microstructures driving overall trends. With more granular data come sharper, more accurate forecasts. When combined with focused historical training sets, these granular inputs outperform broad aggregates, all else equal.

______________________________________________________

[1] Securities finance modeling, when properly tuned, taps into a controlled environment. Unlike open systems, the interplay of factors is more limited, making it easier to isolate signals that matter. Existing studies demonstrate that narrowing variables enhances precision (see Adrian and Shin, “Financial Intermediaries and Monetary Economics,” in Handbook of Monetary Economics, 2010, and Duffie, Measuring Corporate Default Risk, Oxford University Press, 2011).