Data Engineering by Dan Hammond

“More data and transparency are good, but it would be helpful to know what it will be used for.” That point was raised by a panelist at a recent securities finance industry conference. It’s a good question! We all know why the regulators want transparency, but the panel was talking about the potential impact on the industry from the upcoming securities lenders’ SLATE public disclosures by FINRA.

In just about 18 months, institutional securities lenders will have to file detailed reports with the SEC about their securities loans. Analysts for stock borrowers, using the publicly available data from those reports, will be able to track and compare their costs to borrow securities from different lending agents[1]. Lenders will use the public data to benchmark the revenue from their loans. Lending agents will use the array of cost elements in the data to calibrate their pricing models at slightly off than the midpoint rate for each issue. That rate will be to the lender’s advantage when adjusted for collateral type, term and counterparty risk.

DEFINING THE GOLDILOCKS RATE: BEYOND MEAT, INC. (BYND: MAY 2024)

As a rule, the midpoint of that tranche, the second highest spread category, will be the Goldilocks rate for both lender and borrower. The rebate rate should not be so low as to repel new borrowers with cash to post as collateral. Neither should the rebate rate be so high that lenders will want to recall and reallocate their shares to other borrowers who are willing to take slightly lower rebates on their cash collateral.

The spread between the pool yield and the intrinsic rate for the security is the key management metric. Set it just right and the net cash flow will react to a) the issue’s pricing elasticity of each available position’s relative rebate appeal to new borrowers in comparison to b) the relative distaste of the new, higher spread, with lower rebate, to “older” borrowers.

This technology and public data dump doesn’t come for free. Lenders are expected to pay for the reporting structure, as well as for the use of their own data from FINRA if they wish to calibrate their own risk models. Lending agents will be expected to shift that precise Goldilocks, mid-point rate position in anticipation of each day’s changing diffusion of rebate rates. The revenue impact for lenders can be significant and will be explained in a later blog.

THERE ARE NO EASY CORRELATIONS

As observed above, periods of high lending volumes don’t always correlate to lower stock prices or even higher trends in loan fees. While there were many periods of challenging price discovery, fees and volumes often rose in advance of declining stock prices, as illustrated in mid-2022 and mid- and late 2023, showing the information advantage of price leaders. Fees did not always rise during the highest loan volume periods, even when availability buffers were near depletion, suggesting agent-lender difficulty in price discovery or their reluctance to rerate loans with favored borrowers.

Agents that could more precisely price loan fees using a Goldilocks rate could stay ahead of high volatility. Obviously, maintaining the mid-point of the 2nd tranche will require a prediction of the next day’s array of loan rebate rates. Fortunately for lending agents, generative AI technology will enable forecasters to use public data for calibrating their models, thus enabling very accurate predictions for the first time. Deep learning AI models, designed for securities finance as a closed system constrained by capital and collateral, can be trained with a combination of private and public data to make ever more precise rate forecasts, as will also be explained in a later blog.

Sustainable, Above-Average Revenues from Precision Pricing

Securities finance is a market partnership among lenders, borrowers and their intermediaries. Critics of securities lending claim that borrowers and lenders have opposing interests, i.e., that borrowers make money when security prices fall in a lender’s portfolio. Conversely, borrowers lose money, critics say, when lenders win. However, that’s too simplistic because both make money during the lifecycle of a securities loan. For example, long-term lenders earn rental fees for their portfolios when falling prices give capital gains to borrowers. The goal is to make sure that loans are priced fairly and the lender-borrower partnership is managed equitably. Precision pricing is the way to achieve that, as illustrated by a case study using equity loans of Beyond Meat, Inc. (BYND) a stock in great demand from borrowers.

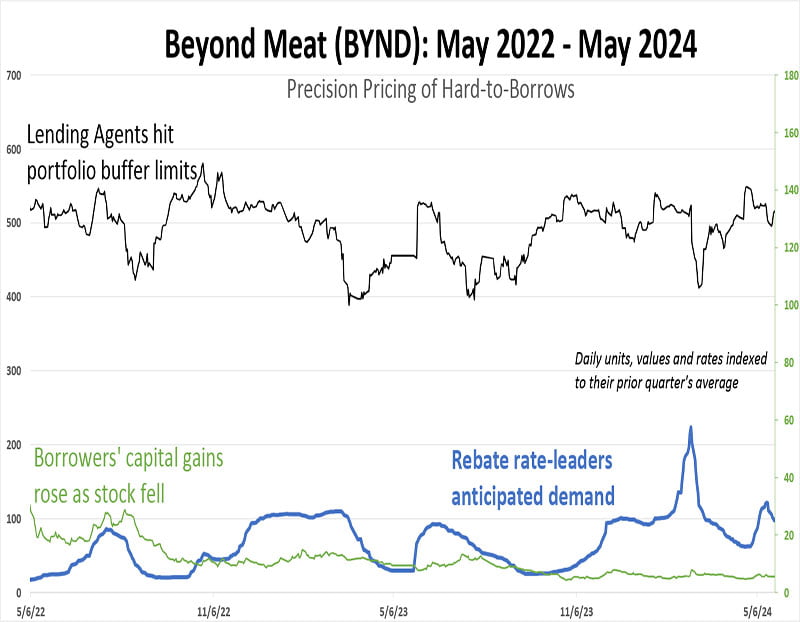

THE BYND STORY: SOARING, UNMET EXPECTATIONS

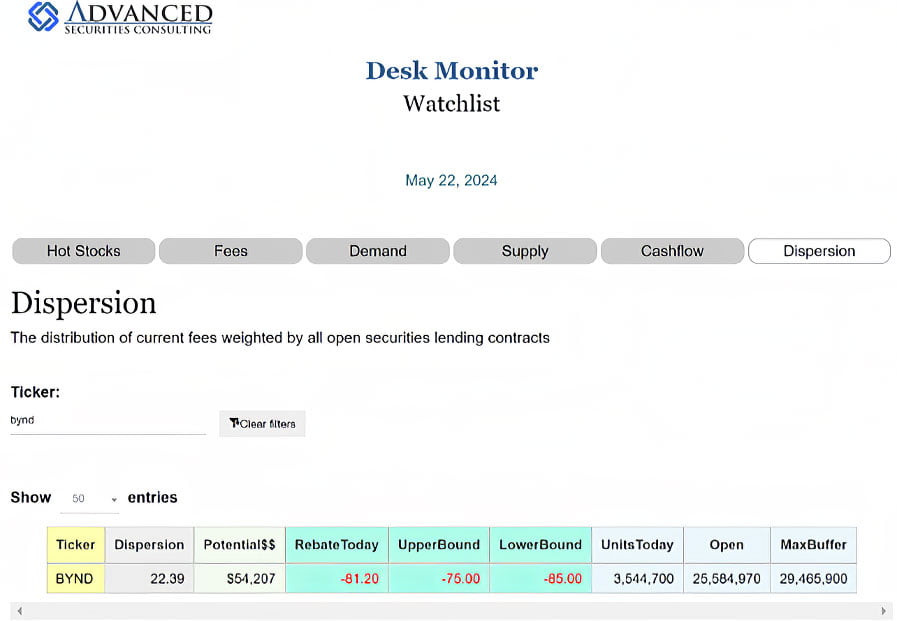

ASC’s Desk Monitor reports current rates, dispersion, volumes, and revenue opportunities.

In June 2019, one month after its initial public offering, Beyond Meat (BYND) was priced at $202 share. The price dropped through 2019 but recovered during the 2020 covid focus on healthy lifestyles. On January 1, 2021, the stock price was still above $175. However, a long slide then began. The stock hit $15 on October 1st.

Fees for borrowing BYND were not abusive during the slide, but remained relatively low and stable until May of 2022, when demand for loans began rising. Rebates on cash collateral were cut to meet rising demand, shown on the chart as an increase in outstanding loan positions. At that point, portfolio buffers started to become a consideration for borrowers of BNYD.

The stock became hard to borrow in the financing markets, limiting the ability of short sellers to execute their trades. Lending agents reacted to demand, and the best agents made loans that consistently achieved returns above the average. Those agents set their rates slightly above the average, in the Goldilocks zone, to produce returns above the benchmarks for each category of collateral.

PROTOTYPE FORECASTS USING AGGREGATES

Securities lenders and their agents can use SLATE data for precision pricing in the context of ‘anticipated’ market moves. Their models will have to forecast share volume and direction within a complicated feature set, derived by a matrix calculus of supply and demand factors. However, feature engineers take comfort: the securities finance market is a bounded network of intermediaries who are each limited by constraints imposed by their collateral, policies and net capital rules, among other binding constraints. That means that, exploiting the calibration benefits from the SLATE public disclosures, agents can predict cash flows and their relation to fees in securities finance for the first time.

Daily forecasts using data from Tidal Markets LLC

Daily forecasts using data from Tidal Markets LLC

OVERCOMING THE LIMITS OF PUBLIC DATA

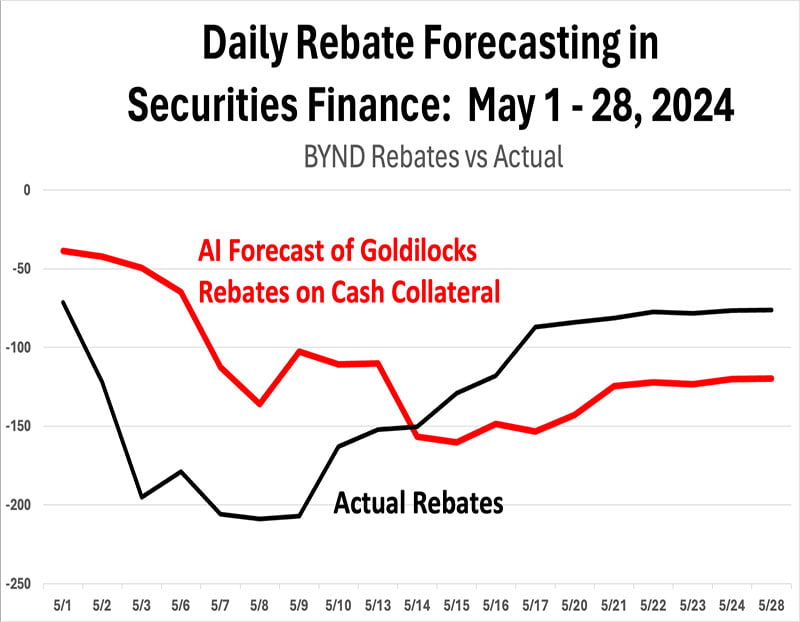

Although the volume of shares within rate buckets from SLATE will not be made available for 21 days, savvy lenders can correlate their activity from the daily SLATE data and estimate the missing volumes. That will suit the generative AI models, if they have fifteen months of a balanced training dataframe for predictive data analytics. Clearly, the eighteen months until SLATE activation does not leave much time to accumulate data and experience at those lending agents that have not started their model building.

Advanced Securities Consulting has been working on predictive analytics for over ten years. The above chart illustrates the results of the best of five neural network models in forecasting BYND rebate movements. As the best model continued learning from the training data, its directional accuracy improved in 14 of the last 19 forecasts. Even better, the magnitude of the mean absolute error narrowed between the actual and predicted values.